Ireland is recognised as one of the most open economies in the developed world. Notwithstanding ongoing moves towards the globalisation of corporate taxes, Ireland continues to attract foreign direct investment (FDI).

WHY SET UP IN IRELAND

Ireland’s international competitiveness is built on strong foundations, including:

- A 12.5% corporate tax rate on trading activities;

- Generous tax reliefs for technology companies, including the Research & Development (R&D) Tax Credit and the Knowledge Development Box;

- A wide network of international tax treaties, which are central to attracting FDI;

- An educated workforce, who speak English as a first language;

- A great location on the edge of Europe, and a member of the European Union.

In recent years, there has been exponential growth in the tech sector in Ireland, both from foreign companies investing in Ireland, and within the domestic economy. In this article, we explore the generous tax relief available to tech companies -- the R&D tax credit.

From our experience, companies in the following industries are ideally suited to best avail of these reliefs and are thriving in the knowledge economy in Ireland at present:

- IT – Software and Hardware;

- Pharmaceutical & Medical Devices;

- Design & Manufacturing;

- Engineering;

- Construction & Architecture.

RESEARCH & DEVELOPMENT TAX CREDIT

The Research & Development (“R&D”) Tax Credit is a lucrative incentive aimed at promoting expenditure on R&D activities by Irish resident companies and branches of foreign companies. The R&D Tax Credit is a valuable relief, and this brochure summarises the incentive, enabling companies to establish whether your business might be entitled to relief under the regime.

QUALIFYING COMPANY

Before reviewing the activities being carried on by a company, first consideration should be given to the requirements to be considered a “qualified company”.

A company is eligible for relief where it is:

- Within the charge to Irish corporation tax;

- Carrying on a trade or is a member of a trading group;

- Carrying out qualifying R&D activities in the period;

Where a trading company within the charge to Irish corporation tax engages in R&D, it may be entitled to claim the R&D Tax Credit in respect of eligible expenditure incurred in the period.

QUALIFYING ACTIVITIES

For research or development efforts to be eligible for relief under the R&D Tax Credit regime, activities must be systematic, investigative or experimental, in a field of science or technology, and be describable under one or more of the following headings:

- Basic research; often blue-sky thinking;

- Applied research; generally what we consider traditional R&D, i.e., labs and white coats; or,

- Experimental development; from our experience, most R&D claims fall within this category. The aim often being to bring a product or solution to market, building on earlier basic or applied research.

Activities will not be considered qualifying unless they seek to advance existing scientific or technological knowledge and involve the resolution of a scientific or technological uncertainty.

QUALIFYING EXPENDITURE

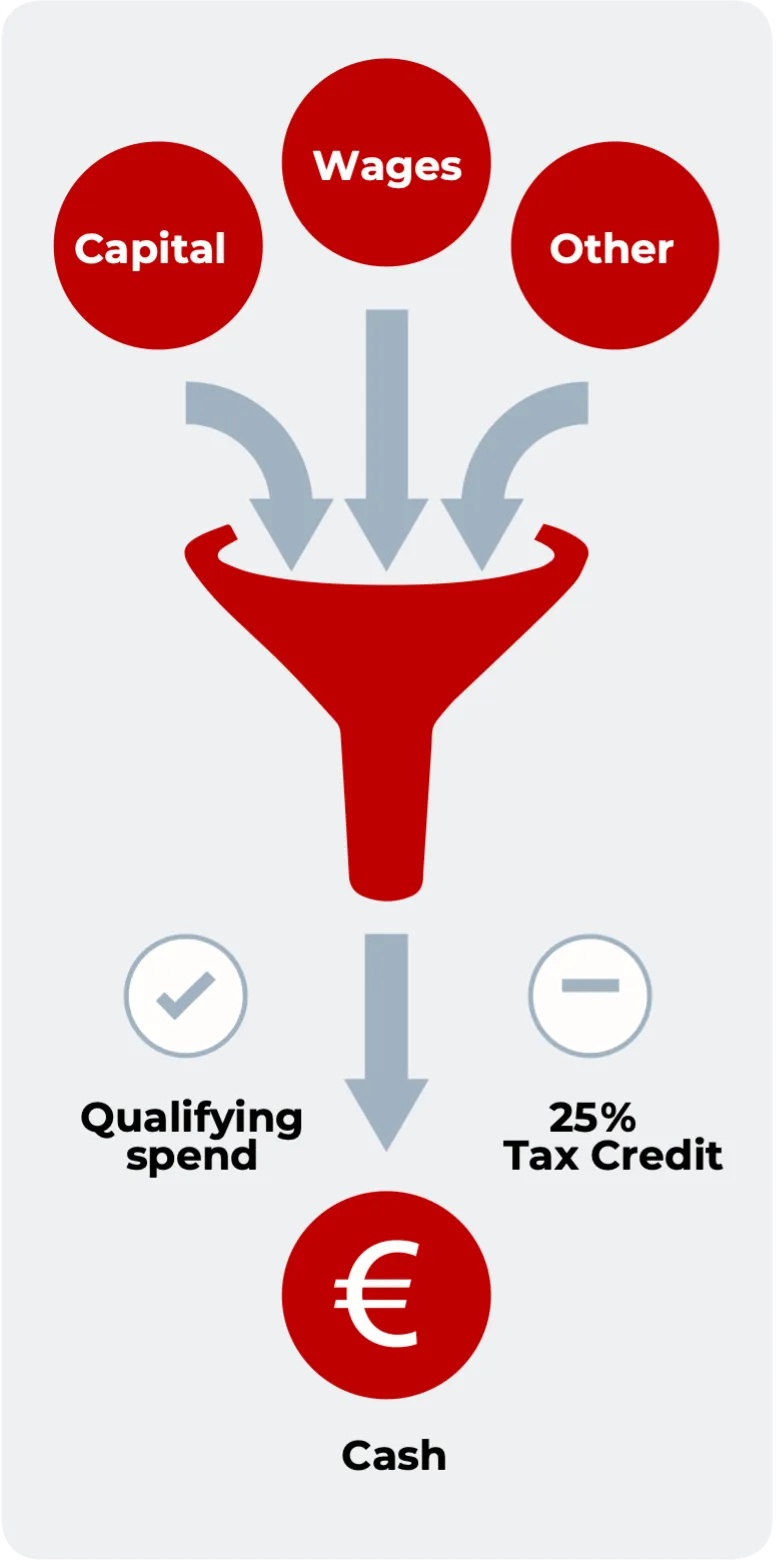

Eligible expenditure is determined by reference to the activities carried on by a company and typically includes:

- Wages and salaries (fully loaded, to include bonuses, pension, health insurance, etc.),

- Direct overheads such as light and heat, direct facility costs such as rent and maintenance,

- Direct costs, including materials used in the course of the R&D activities being carried out,

- Sub-contractors and third-level institutions may also be included in the claim; however, there are limits as to the amount of expenditure which may be included.

In addition to Revenue expenditure, a claim can include expenditure on plant and machinery to the extent that the assets are used for the R&D effort, once the assets are eligible for capital allowances.

Likewise, the capital cost of buildings may be included in a claim in the year of expenditure, to the extent that a facility is purpose built to facilitate R&D activities.

CLAIMING THE CREDIT

The R&D Tax Credit regime operates on a self-assessment basis, submitted on the Form CT1 form the period in which the qualifying expenditure is incurred.

A claim must be submitted to Revenue within 12 months of the end of the accounting period in which the expenditure was insured. Timeliness of claims is therefore imperative.

UTLISING THE CREDIT

First, the R&D Tax Credit can be used to reduce a company’s current year corporation tax liability, or can be carried back to the generate a refund of corporation tax paid in the immediately preceding accounting year.

Once Corporation Tax offsets have been exhausted, a company may then choose to either carry the credit forward or elect for a refund of the remaining credit over a three year period, by reference to payroll taxes paid.

TAKE AWAYS

- R&D tax credits at 25% of qualifying expenditure, in addition to a 12.5% Corporation Tax deduction.

- Qualifying expenditure includes fully loaded wages, subcontractors, direct and overhead costs, and capital expenditures.

- Refundable credit, loss making companies may also get a cash benefit.

- Not just white coats – credit is aimed at problem solving disciplines, seeking an improvement on the norm.

- Software and IT are key areas for R&D claims in Ireland.

- Claim must be made within 12 months of end of accounting period.

“The R&D Tax Credit is an incentive which provides a refundable tax credit of 25% of qualifying expenditure carried out in a period. The credit is in addition to the usual corporation tax deductions and capital allowances claims, such that the total tax saving is potentially 37.5%.”

Explore Tax Relief in Ireland

Hughes Tax & Advisory is a boutique tax practice principally serving the needs of Irish businesses and entrepreneurs. Their blend of corporate and personal experience allows their advisors to understand, address and meet the needs of both the entrepreneur and also their companies, to deliver bespoke tax solutions.

Connect with James to inquire about taxes in Ireland and how he can help ease the burden.